FinancialGauge

Independent Strategic Thinking

July 2012

Union of Unequals

Common currency with different outcomes

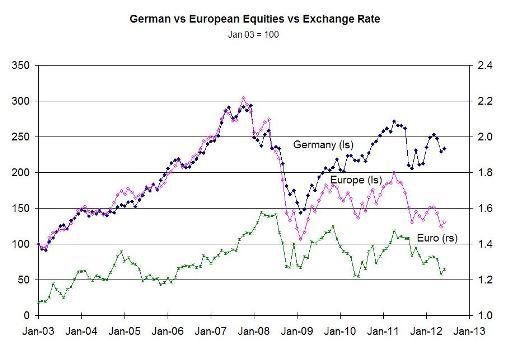

During the boom years from 2003 till the financial collapse at the end of 2007 European equities as well as the Euro all appreciated significantly. Since then, however, German equities have followed their own upward path while European equities overall, and the Euro, are again at or below 2008/09 levels. The difference lies in the restructuring and streamlining of German industry and labor markets that occurred over the past 10 to 15 years, much like the US experience during the 80’s and 90’s, in contrast to the rest of Europe. German companies have thus been the unintended beneficiaries of Europe’s problems in the form of a much weaker Euro and even greater competitiveness.

Strategic Implications:

Notwithstanding the complicated interplay between currency and equity markets, equities ultimately dominate returns.* This suggests that only structural changes in the rest of Europe increasing competitiveness, not currency moves reflecting monetary or fiscal policy, will again make European equities attractive overall.

* Yoav Benari, “When is Hedging Foreign Assets Effective?” The Journal of Portfolio Management, fall 1991.

|

This article is distributed for informational purposes only. All information contained herein should not be considered as investment advice or a recommendation of any particular strategy, security, investment product or financial instrument. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed.

|

|